Family Farm SuccessionFeatures

October 19, 2019

October 19, 2019

How to create a succession plan: 10 elements you need to include

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Transitioning the poultry farm to the fourth generation

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Darrell Wade is the 2017 Wilson Loree Award winner

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

A different approach to succession

Advertisement

Stories continue below

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Treating succession planning as a process, not an event

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Succession planning: What you need to know from a management consultant

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

How to write a will joyfully

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Dealing with retiring farmers to create landlord relationships

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Avoid the mistakes farmers typically make

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Tips for choosing a successor for the family farm

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Tips for young farmers: Getting started on farm transition planning

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Succession advice from farm families

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Focusing on finance – not just the farm

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Financial support for young farmers a barrier for transition

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

The importance of starting a succession plan early

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

Your transition team: who you need on your side to develop a succession plan

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

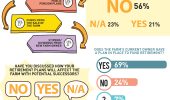

92% of farms have no succession plan in place – putting family farms at risk

Family Farm SuccessionFeatures

October 17, 2019

October 17, 2019

New study: Two thirds of farmers question if their children should farm

Family Farm SuccessionFeatures

June 13, 2019

June 13, 2019

Funding the future: Discussing retirement in transition planning

Family Farm SuccessionFeatures

June 12, 2019

June 12, 2019

Finances before transition?

Family Farm SuccessionFeatures

May 17, 2019

May 17, 2019

How are we learning about succession planning?

Family Farm SuccessionFeatures

May 17, 2019

May 17, 2019

Who owns the farm and who will own the farm?

Family Farm SuccessionFeatures

May 17, 2019

May 17, 2019

Are we talking about succession planning?

Family Farm SuccessionFeatures

May 17, 2019

May 17, 2019

The state of succession

Family Farm SuccessionFeatures

May 17, 2019

May 17, 2019

Dealing with dynamics

Family Farm SuccessionFeatures

May 15, 2019

May 15, 2019

Who answered the Ag Succession Survey?

Family Farm SuccessionFeatures

October 17, 2018

October 17, 2018

Do’s and Dont’s for farm succession

Family Farm SuccessionFeatures

October 17, 2017

October 17, 2017

7 legal considerations for succession planning

Family Farm SuccessionFeatures

October 17, 2017

October 17, 2017

Finance and tax advice for succession planning

Family Farm SuccessionFeatures

October 17, 2017

October 17, 2017

From farm kid to farm owner: how to transition to ownership

Family Farm SuccessionFeatures

October 17, 2017

October 17, 2017

Succession Planning: Resource round-up

Family Farm SuccessionFeatures

October 17, 2017